If you’ve been exploring different home loan options, you may have come across the term balloon payment mortgage. At first glance, it might sound simple — smaller payments now, one large payment later. But as with most financial decisions, there’s more to the story.

If you’re wondering whether this mortgage could work for you, you’re in the right place. Let’s break it down in plain English so you can make a confident, informed decision.

What Is a Balloon Payment Mortgage?

A balloon payment mortgage is a type of home loan that offers lower monthly payments for a set period of time — usually 5 to 7 years — followed by one large payment (the “balloon”) at the end of the term.

Unlike traditional 15-year or 30-year fixed-rate mortgages, this mortgages don’t fully amortize over the loan term. That means you’re not paying off the entire principal balance through monthly payments alone. Instead, a significant portion remains due in one lump sum.

Here’s a simple example:

- Loan amount: $300,000

- Term: 5 years

- Monthly payments calculated as if it were a 30-year mortgage

- After 5 years, the remaining balance (possibly $250,000+) becomes due all at once

That final large payment is the balloon payment.

How Do Balloon Mortgages Work?

Most balloon payment mortgages follow this structure:

- Initial period (5–7 years)

You make relatively low monthly payments. These may cover only interest (interest-only balloon mortgage) or both principal and interest, but calculated over a longer amortization schedule. - Balloon payment due date

At the end of the term, the remaining balance must be paid in full.

This can be done in one of three ways:

- Paying the full balance in cash

- Selling the property

- Refinancing into a new mortgage

If none of these options are possible, you could face serious financial strain — which is why understanding the risks is critical.

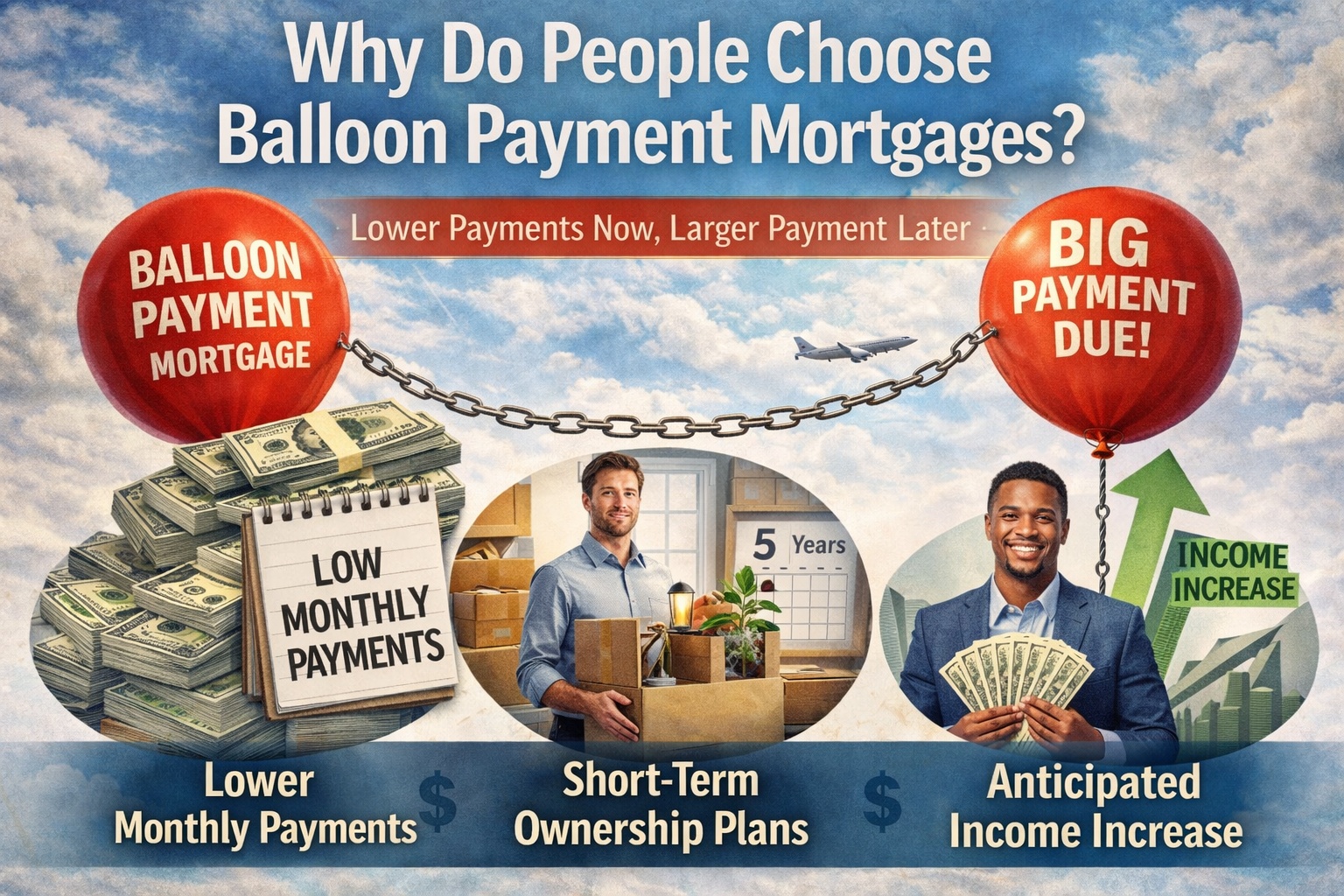

Why Do People Choose Balloon Payment Mortgages?

At first glance, the idea of a large future payment might sound stressful. But there are situations where this mortgage actually makes sense.

1. Lower Monthly Payments

Because payments are calculated over a longer period (like 30 years), your monthly costs are typically lower than with a short-term fixed loan.

If you need short-term cash flow flexibility, this can be appealing.

2. Short-Term Ownership Plans

If you plan to:

- Sell the home within a few years

- Relocate for work

- Flip the property

A balloon payment mortgage may align with your timeline.

3. Anticipated Income Increase

Some borrowers expect a significant income boost — perhaps from a business expansion, inheritance, or career progression — and believe they’ll be able to handle this type of payment later.

But this is where caution becomes important.

The Risks of Balloon Payment Mortgages

Let’s be honest — This mortgages aren’t for everyone. And they can be risky if you’re not fully prepared.

1. Large Lump-Sum Payment

The biggest concern is obvious: that large final payment.

If you’re unable to refinance or sell your home before the payment is due, you could face foreclosure.

2. Refinancing Isn’t Guaranteed

Many borrowers assume they’ll simply refinance when the balloon comes due. But refinancing depends on:

- Your credit score

- Market conditions

- Interest rates

- Property value

If rates have increased or your financial situation has changed, refinancing may not be easy — or affordable.

3. Market Uncertainty

If home values drop and you owe more than the property is worth, selling the home may not cover the balloon balance.

This is why balloon mortgages are generally considered higher-risk home loan options.

Balloon Mortgage vs. Traditional Mortgage

Let’s compare the two.

| Feature | Balloon Mortgage | Traditional Mortgage |

|---|---|---|

| Monthly Payments | Lower (initially) | Consistent |

| Loan Term | Short (5–7 years) | 15–30 years |

| Final Payment | Large lump sum | Fully paid off over time |

| Risk Level | Higher | Lower |

A traditional fixed-rate mortgage offers long-term predictability. This mortgage offers short-term savings with long-term uncertainty.

It really comes down to your financial strategy and risk tolerance.

Types of Balloon Payment Mortgages

Not all loans are identical. Here are a few variations:

Interest-Only Balloon Mortgage

You pay only interest during the initial term. The entire principal balance is due at the end.

This results in the lowest monthly payments — but the highest final balloon amount.

Partially Amortized Balloon Mortgage

You pay principal and interest, but based on a longer amortization schedule (like 30 years), even though the loan term is shorter.

This reduces the amount slightly.

Fixed-Rate vs. Adjustable-Rate Balloon

Some of this mortgages have fixed interest rates, while others may adjust over time.

Always read the fine print carefully.

When Might a Balloon Mortgage Be a Smart Choice?

Let’s say you’re:

- A real estate investor flipping properties

- A business owner expecting large future revenue

- Planning to relocate within 3–5 years

- Purchasing land or short-term investment property

In these cases, this payment mortgage could serve as a strategic financing tool.

But if you’re buying your forever home and prefer stability, a traditional mortgage may be the safer route.

Questions You Should Ask Before Choosing a Balloon Mortgage

Before signing anything, ask yourself:

- What is my exit strategy? (Sell or refinance?)

- Can I realistically afford this type of payment?

- What happens if property values fall?

- What if interest rates rise?

- Do I have backup savings?

If you don’t have clear answers, pause and reconsider.

Tips for Managing a Balloon Payment Mortgage

If you decide to move forward with this type of loan, here are some smart strategies:

1. Start Preparing Early

Don’t wait until year five to think about refinancing. Begin reviewing your options at least 12–18 months before the balloon payment is due.

2. Build an Emergency Fund

Having savings gives you flexibility if the housing market shifts unexpectedly.

3. Monitor Your Credit Score

A strong credit profile improves refinancing opportunities.

4. Watch Market Trends

Stay informed about interest rates and local housing values.

Is a Balloon Mortgage Right for You?

Here’s the honest answer: it depends.

This payment mortgage can be helpful in the right situation. But it requires careful planning and financial discipline.

If you:

- Value predictability

- Don’t want refinancing pressure

- Plan to stay in your home long-term

You may prefer a fixed-rate mortgage.

If you:

- Have a clear short-term plan

- Understand the risks

- Are financially flexible

It might be worth considering.

Final Thoughts on Balloon Payment Mortgages

Choosing the right home loan isn’t just about today’s monthly payment — it’s about your long-term financial stability.

This payment mortgages offer flexibility and lower initial payments, but they also introduce risk and uncertainty. The key is having a solid plan before the payment arrives.

Before making any decision, speak with a qualified mortgage professional who can assess your personal financial situation.

And while you’re researching smart financial strategies, you may also enjoy exploring additional lifestyle and finance-related insights at:

These resources offer a variety of articles designed to keep you informed and inspired.

Bottom Line

A balloon payment mortgage can be a powerful tool — or a financial burden — depending on how you use it.

Take your time. Run the numbers. Think about your future plans. And most importantly, make a decision that aligns with your long-term goals.

Because at the end of the day, your home should bring peace of mind — not financial stress.