Buying or selling a home is often described as one of the biggest milestones in a person’s life. It’s exciting, emotional, sometimes overwhelming—and if we’re being honest, a little confusing too. Somewhere between house hunting, inspections, negotiations, and paperwork, you’ll hear a phrase that can feel both vague and intimidating: closing costs.

If you’re buying or selling a home in Indiana, understanding closing costs isn’t just helpful—it’s essential. These aren’t small, forgettable fees. They can add up to thousands of dollars, and if you’re not prepared, they can catch you off guard at the worst possible moment.

This guide isn’t just about listing fees. It’s about helping you actually understand what’s happening, why these costs exist, and how they impact you as a buyer or seller in Indiana. Think of this as the conversation you wish someone had with you before closing day.

What Are Closing Costs, Really?

Closing fees and expenses you pay when finalizing a real estate transaction. This happens on closing day—the day ownership officially transfers.

In Indiana, closing costs typically range:

- Buyers: ~2% to 5% of the home’s purchase price

- Sellers: ~6% to 10% (mostly due to agent commissions)

So, if you’re buying a $250,000 home, you might pay around $5,000 to $12,500 in closing costs. Sellers, on the other hand, could pay $15,000 to $25,000 or more.

That’s not pocket change—and that’s why understanding each piece matters.

Why Closing Costs Feel So Complicated

Here’s the honest truth: closing costs feel confusing because they’re not just one thing. They’re a collection of:

- Government fees

- Lender charges

- Insurance premiums

- Service provider costs

- Prepaid expenses

And each of these is handled by different parties. Some are negotiable, others are not. Some are one-time fees, others are tied to ongoing obligations.

It’s like paying for a concert ticket and then discovering there are fees for parking, service charges, merchandise, and snacks—all bundled at the end.

Closing Costs for Buyers in Indiana (Full Breakdown)

Let’s break this down in a way that actually makes sense.

1. Loan-Related Fees

If you’re financing your home, this is where a big portion of your closing costs comes from.

Loan Origination Fee

This is what your lender charges for processing your loan.

- Typical cost: 0.5% to 1% of loan amount

This fee covers underwriting, paperwork, and basically the lender’s effort to get your loan approved.

Credit Report Fee

Lenders check your credit history.

- Typical cost: $25 to $50

Small, but unavoidable.

Appraisal Fee

Before lending you money, the lender needs to know the home is worth it.

- Typical cost in Indiana: $400 to $600

This ensures you’re not overpaying—and that the bank isn’t over-lending.

Discount Points (Optional)

You can pay upfront to lower your interest rate.

- 1 point = 1% of your loan

This is optional, but sometimes worth it if you plan to stay long-term.

2. Title and Settlement Fees

Indiana uses title companies (not attorneys, in most cases) to handle closings.

Title Search

This checks if the property has legal issues—like unpaid taxes or liens.

- Typical cost: $150 to $300

Title Insurance

This protects you (and your lender) from ownership disputes.

- Lender’s policy: Required

- Owner’s policy: Optional but strongly recommended

- Typical cost: $1,000 to $2,000+

It’s a one-time fee, but it protects you for as long as you own the home.

Settlement / Closing Fee

This pays the title company for coordinating everything.

- Typical cost: $200 to $500

3. Prepaid Costs (The Sneaky Ones)

These often surprise buyers the most.

Property Taxes (Prepaid Portion)

In Indiana, property taxes are paid in arrears (you pay for the previous period).

At closing, you may need to prepay your share depending on timing.

Homeowners Insurance

Lenders require you to pay at least the first year upfront.

- Typical cost: $800 to $1,500 annually

Escrow Account Funding

Your lender may require you to deposit several months of:

- Property taxes

- Insurance

This can be $1,000 to $3,000+, depending on your home.

4. Recording Fees

These are government fees to officially record the transaction.

- Typical cost in Indiana: $50 to $150

5. Inspection Fees (Technically Pre-Closing)

While not always listed as closing costs, they’re part of the process.

- Home inspection: $300 to $500

- Pest inspection: $75 to $150

Closing Costs for Sellers in Indiana

Now let’s talk about the other side of the table.

1. Real Estate Agent Commissions

This is the biggest cost for sellers.

- Typical: 5% to 6% of sale price

This is split between:

- Listing agent

- Buyer’s agent

On a $250,000 home, that’s about $12,500 to $15,000.

2. Title Fees (Seller Portion)

In Indiana, sellers often pay for:

- Owner’s title insurance

- Title services

- Typical cost: $1,000 to $2,500

3. Transfer Taxes (Minimal in Indiana)

Good news: Indiana has relatively low transfer taxes compared to other states.

- Rough estimate: $0.50 per $500 of property value

4. Prorated Property Taxes

Since taxes are paid in arrears, sellers usually credit the buyer for their portion.

5. Repairs or Credits

If issues come up during inspection, sellers might:

- Pay for repairs

- Offer closing credits

This varies widely.

6. Mortgage Payoff

If you still owe on your home, your lender gets paid at closing.

Who Pays What? (Indiana Norms)

While everything is technically negotiable, here’s the typical breakdown:

Buyer Usually Pays:

- Loan fees

- Appraisal

- Credit report

- Home inspection

- Lender’s title insurance

- Escrow/prepaids

Seller Usually Pays:

- Agent commissions

- Owner’s title insurance

- Some title fees

- Property tax prorations

The Emotional Side of Closing Costs

Let’s step away from numbers for a moment.

Closing costs can feel frustrating, especially when you’ve already:

- Saved for a down payment

- Budgeted for moving

- Invested emotionally in the home

And then suddenly, there’s another $8,000 you didn’t fully expect.

It’s normal to feel:

- Overwhelmed

- Irritated

- Even a little blindsided

But here’s the perspective that helps: these costs are part of making the deal real. They ensure:

- The home is legally yours

- The title is clean

- The lender is protected

- The transaction is recorded properly

In a way, closing costs are the “infrastructure” behind your homeownership.

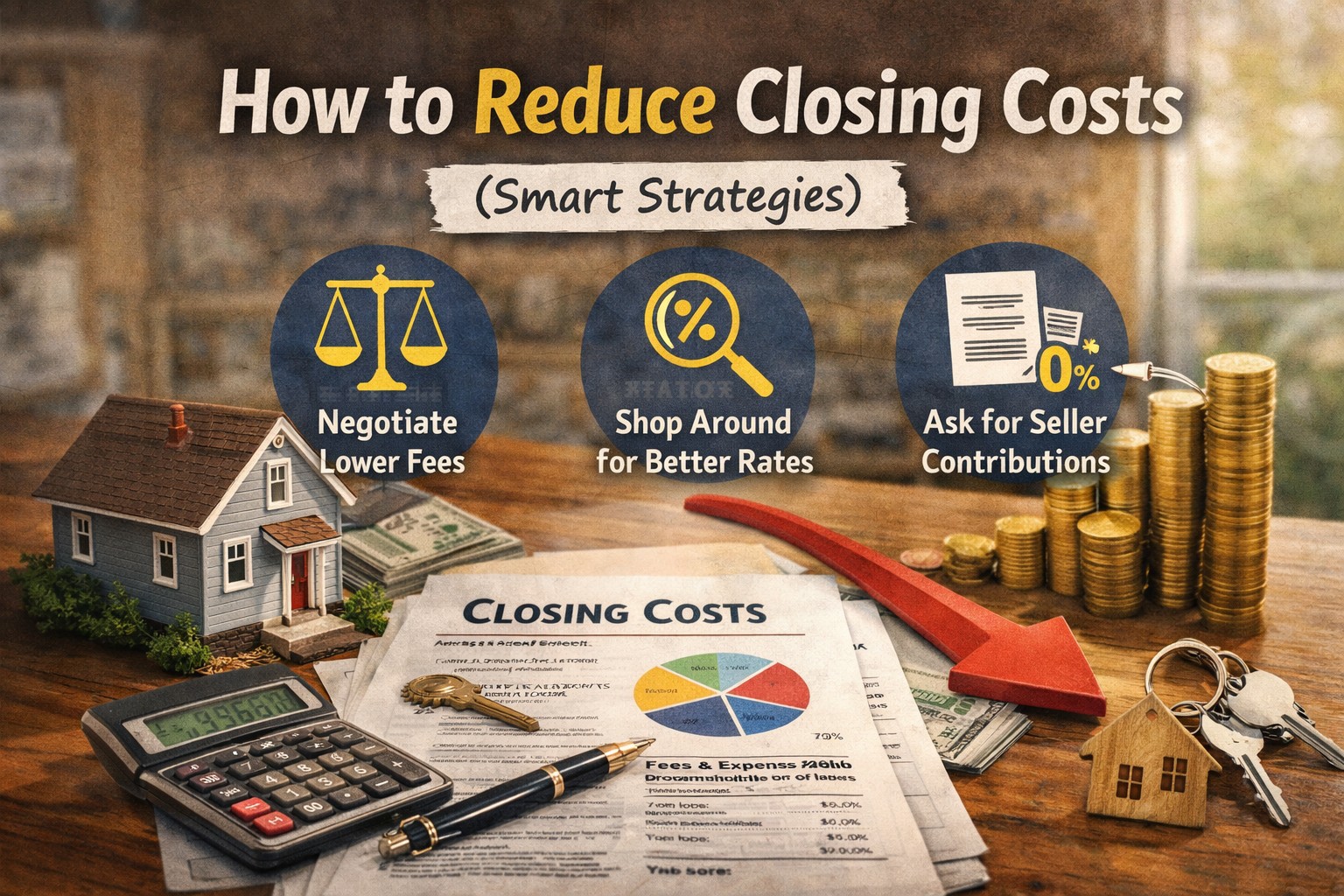

How to Reduce Closing Costs (Smart Strategies)

You don’t always have to accept everything as-is.

1. Shop Around for Lenders

Different lenders offer different fees.

Even a small difference in:

- Origination fees

- Interest rates

…can save you thousands.

2. Ask for Seller Concessions

You can negotiate for the seller to cover part of your closing costs.

- Common in buyer-friendly markets

- Typically 2% to 3% of purchase price

3. Compare Title Companies

Not all title companies charge the same.

4. Close at the End of the Month

This reduces prepaid interest.

5. Review the Loan Estimate Carefully

Your lender is required to provide a Loan Estimate early on.

Compare it with your Closing Disclosure before closing.

What Is a Closing Disclosure?

A few days before closing, you’ll receive this document.

It includes:

- Final loan terms

- Exact closing costs

- Cash needed at closing

Take your time reviewing it. Ask questions. This is your moment to catch mistakes or unexpected charges.

A Real-Life Example (Indiana Buyer)

Let’s say you’re buying a home in Indianapolis for $300,000.

Here’s what your closing costs might look like:

- Loan origination: $2,400

- Appraisal: $500

- Title insurance: $1,800

- Escrow/prepaids: $2,500

- Misc fees: $800

Total: ~$8,000

Now imagine walking into closing knowing this number ahead of time versus being surprised by it. That difference alone changes your entire experience.

Common Mistakes to Avoid

1. Not Budgeting Enough

Always assume the higher end of estimates.

2. Ignoring Prepaids

These aren’t “fees,” but they still require cash upfront.

3. Not Asking Questions

No question is too small when thousands of dollars are involved.

4. Waiting Until the Last Minute

Review documents early.

Why Indiana Is Unique

Indiana is considered relatively affordable when it comes to closing costs compared to other states.

Reasons include:

- Lower property taxes (in many areas)

- Minimal transfer taxes

- Title company-based closings (less attorney involvement)

That said, “affordable” doesn’t mean “cheap”—you still need to prepare.

Final Thoughts: It’s More Than Just Fees

Closing costs can feel like a final hurdle—but they’re also the final step before something meaningful:

- Your first home

- A fresh start

- A new chapter

When you understand what you’re paying for, it shifts from feeling like a burden to feeling like part of the process.

You’re not just paying fees—you’re securing ownership, protecting your investment, and completing a journey that likely took months (or years) to reach.

If You Remember Only One Thing

Closing costs aren’t random—they’re predictable.

And when something is predictable, you can plan for it, negotiate it, and handle it with confidence.