If you’ve ever borrowed money or helped someone secure a loan, you may have heard the term “equitable mortgage.” It sounds complicated, but the concept is actually easier to understand than you might think. And if you live in Indiana or are dealing with property there, knowing how an equitable mortgage in Indiana works could save you from legal confusion or costly mistakes.

In this guide, we’ll break everything down in simple terms—what an equitable mortgage is, how Indiana courts treat it, and what you should watch out for if you’re involved in a property-related loan.

Let’s dive in.

What Is an Equitable Mortgage?

An equitable mortgage is a type of mortgage recognized by courts based on the intent of the parties involved, even if a formal mortgage document was never created.

In simple terms, this mortgage happens when:

- Someone borrows money

- Property is used as security for the loan

- But the paperwork doesn’t technically create a standard mortgage

Despite the lack of formal documentation, the court may still treat the arrangement as a real mortgage because the intention was clearly to secure a loan with property.

This concept exists to prevent unfair situations where someone tries to avoid repayment simply because a technical requirement wasn’t met.

Why Equitable Mortgages Exist

The purpose of an equitable mortgage is fairness.

Imagine this situation:

- A homeowner borrows money from a friend.

- They promise their house as collateral.

- They sign some informal documents or transfer a deed temporarily.

Later, the borrower refuses to repay the loan and argues that there was never a legal mortgage.

Without the concept of this mortgage, the lender could lose their security entirely.

Courts step in to say:

“If both parties intended the property to secure a loan, we will treat it as a mortgage.”

This protects the lender from unjust outcomes.

How Equitable Mortgages Work in Indiana

Indiana courts recognize the principle of equitable mortgages, but they evaluate each case carefully.

To establish an equitable mortgage in Indiana, courts generally look for clear evidence of intent that the property was meant to secure a debt.

Some factors courts may consider include:

- Written agreements or notes referencing the loan

- Transfer of a property deed intended as security

- Payment records showing a loan arrangement

- Communication between the parties

- Behavior of the borrower and lender

The most important factor is intent. If the evidence shows that both parties intended to create security for a loan, Indiana courts may enforce an equitable mortgage.

Common Situations Where Equitable Mortgages Appear

Equitable mortgages often arise in real-life situations where formal legal steps weren’t followed properly.

Here are some common scenarios.

1. Deed Given as Security for a Loan

Sometimes a borrower transfers the title of a property to the lender as collateral, with the understanding that the title will return once the loan is paid.

If the lender later claims full ownership of the property, a court may rule that the deed was actually meant as security for a loan, creating an equitable mortgage.

2. Informal Loan Agreements

Friends or family members often create handwritten agreements when money is borrowed.

If the document mentions property as collateral but doesn’t meet formal mortgage requirements, courts may still treat it as an equitable mortgage.

3. Mistakes in Mortgage Documentation

Sometimes a mortgage document exists but contains technical defects.

Examples include:

- Improper notarization

- Missing signatures

- Recording issues

If the parties clearly intended to create a mortgage, a court may enforce it under equitable principles.

Legal Elements Courts Look For

If someone claims an equitable mortgage in Indiana, they must prove certain elements.

Although each case is unique, courts typically examine:

1. A Debt or Loan Exists

There must be a real financial obligation between the parties.

Without a debt, there can be no mortgage.

2. Property Was Intended as Security

The borrower must have intended to secure the debt with property.

Intent can be shown through documents, testimony, or behavior.

3. Evidence of the Agreement

Courts prefer clear and convincing evidence.

This might include:

- Emails or text messages

- Loan repayment schedules

- Written agreements

- Witness statements

The stronger the evidence, the easier it is for a court to recognize an equitable mortgage.

Risks of Informal Mortgage Arrangements

While equitable mortgages can protect lenders, relying on them can still be risky.

Informal agreements often lead to disputes, misunderstandings, or legal battles.

Some common problems include:

Unclear Loan Terms

Without formal documentation, parties may disagree about:

- Interest rates

- Payment schedules

- Default consequences

Ownership Conflicts

If a property deed was transferred, disputes about true ownership can arise.

Costly Litigation

Proving an equitable mortgage often requires going to court, which can be expensive and time-consuming.

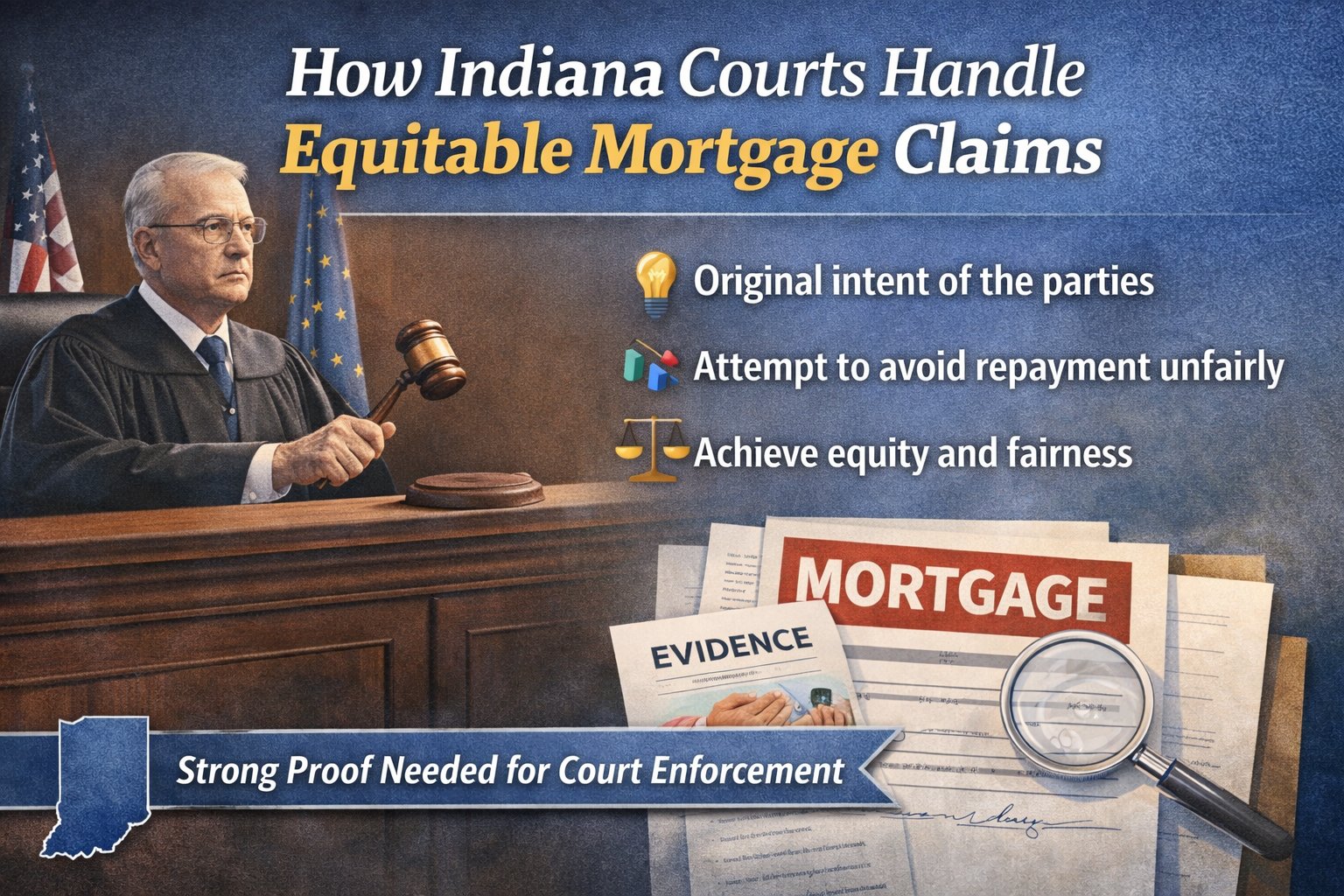

How Indiana Courts Handle Equitable Mortgage Claims

Indiana courts generally approach equitable mortgage claims cautiously.

Because property ownership is a serious legal matter, judges want strong proof before declaring that a mortgage exists.

In many cases, the court examines:

- The original intent of the parties

- Whether the borrower attempted to avoid repayment unfairly

- Whether enforcing the mortgage would achieve equity and fairness

If the evidence supports the claim, the court may treat the arrangement just like a traditional mortgage.

This means the lender may be able to pursue foreclosure if the debt is not repaid.

Equitable Mortgage vs Legal Mortgage

To better understand the concept, it helps to compare the two.

| Legal Mortgage | Equitable Mortgage |

|---|---|

| Formal written agreement | May be informal |

| Recorded with the county | May not be recorded |

| Meets all legal requirements | May have technical defects |

| Created intentionally through legal process | Created through intent and fairness principles |

Even though they differ in form, courts may enforce both if the underlying purpose is the same.

Tips to Avoid Equitable Mortgage Disputes

Whether you’re borrowing money or lending it, taking the right precautions can prevent legal problems later.

Here are some practical tips.

1. Use Formal Mortgage Documents

The best way to avoid disputes is to create a proper mortgage agreement drafted by a professional.

2. Record the Mortgage

Recording the mortgage with the county ensures public notice and protects both parties.

3. Keep Written Records

Always maintain documentation such as:

- Loan agreements

- Payment records

- Communication regarding the loan

4. Consult a Real Estate Attorney

Indiana property law can be complex. A qualified attorney can help structure the transaction correctly from the beginning.

Why Understanding Equitable Mortgages Matters

You might wonder why this topic matters unless you’re directly involved in property lending.

But equitable mortgages appear more often than people realize.

They commonly arise in:

- Family loans secured by property

- Private real estate financing

- Property disputes after informal agreements

- Mistakes in mortgage documentation

Knowing how equitable mortgages in Indiana work can help you recognize potential risks and protect your financial interests.

Final Thoughts

An equitable mortgage in Indiana is essentially the court’s way of ensuring fairness when a property loan arrangement wasn’t documented perfectly.

Even if a formal mortgage doesn’t exist, courts may still enforce the agreement if:

- A real debt exists

- Property was intended as collateral

- There is clear evidence supporting that intent

While equitable mortgages protect lenders from unfair outcomes, relying on them is not ideal. The safest approach is always to use proper legal documentation and professional guidance when property is involved.

If you’re considering lending money secured by property—or borrowing money yourself—it’s worth taking the extra time to structure the deal correctly. Doing so can prevent disputes, protect your property rights, and give you peace of mind.

Quick takeaway:

Equitable mortgages exist to uphold fairness, but clear and formal agreements are always the best way to avoid legal complications.