If you’ve been dreaming about buying a home in Indiana but feel discouraged by the idea of a large down payment, you’re not alone. Many people assume homeownership requires tens of thousands of dollars upfront. The good news? USDA loans in Indiana may make it possible to buy a home with zero down payment.

Yes, really.

The USDA home loan program was created to help individuals and families achieve homeownership in rural and suburban areas. And the best part is that many communities across Indiana qualify—even some you might not expect.

In this guide, we’ll walk through everything you need to know about USDA loans in Indiana, including how they work, who qualifies, and why they could be a smart option if you’re ready to buy a home.

What Is a USDA Loan?

A USDA loan is a government-backed mortgage offered through the United States Department of Agriculture (USDA). The goal of this program is to encourage homeownership in rural and suburban areas by making loans more affordable.

Unlike traditional mortgages, this loans offer several advantages that can make buying a home much easier for qualified buyers.

Here are some of the biggest benefits:

- No down payment required

- Competitive interest rates

- Lower mortgage insurance costs

- Flexible credit requirements

- Available to first-time and repeat homebuyers

For many people in Indiana, this loan program opens doors that might otherwise remain closed.

Why USDA Loans Are Popular in Indiana

Indiana is an ideal state for this financing because of its many rural and suburban communities. While major cities like Indianapolis may not qualify, a surprising number of nearby areas do.

Many towns across counties such as:

- Hendricks County

- Johnson County

- Boone County

- Hancock County

- Shelby County

have eligible areas for USDA home loans in Indiana.

Even properties just outside larger metro areas can qualify. This means you could buy a home with zero down payment while still living close to city amenities, work opportunities, and schools.

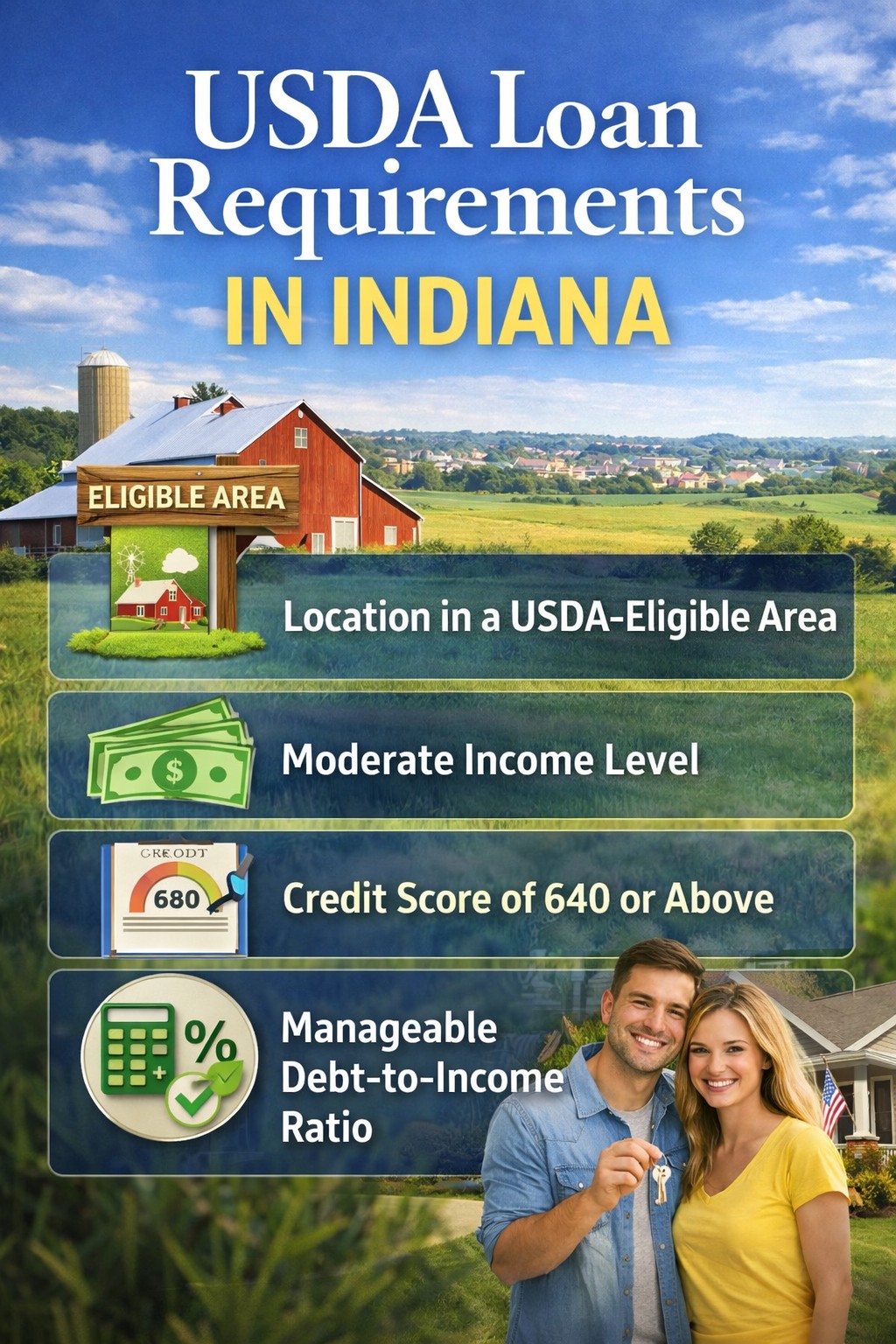

USDA Loan Requirements in Indiana

Like any mortgage program, this loans come with certain eligibility requirements. The good news is they’re generally designed to be accessible.

Let’s break down the key requirements.

1. Location Eligibility

The home must be located in a USDA-eligible rural or suburban area.

Many people assume “rural” means farmland or extremely remote locations, but that’s not necessarily the case. Communities with populations under 35,000 often qualify.

Much of Indiana fits this criteria, making this loans a realistic option for many buyers.

2. Income Limits

This loans are intended to help moderate- and low-income households, so there are income limits based on household size and county.

In many Indiana counties, the general guideline is:

- 1–4 person household: roughly around $110,000 or less

- 5–8 person household: higher limits may apply

Exact limits vary by location, but they are often more flexible than people expect.

3. Credit Score Expectations

While this loan does not set a strict minimum credit score, most lenders prefer:

- 640 or higher for automated approval

However, lower scores may still be approved with additional documentation or manual underwriting.

If your credit isn’t perfect, don’t immediately assume you won’t qualify.

4. Debt-to-Income Ratio

Your debt-to-income ratio (DTI) compares your monthly debt payments to your income.

Typical guidelines include:

- 29% housing ratio

- 41% total debt ratio

That said, lenders sometimes approve higher ratios with strong credit or stable income.

How USDA Loans Work

This loans are different from conventional loans in one key way: they’re backed by the government.

Instead of lending money directly in most cases, the USDA guarantees the loan. This reduces risk for lenders, allowing them to offer better terms to borrowers.

Here’s what that means for you:

- Lower interest rates

- No down payment required

- Reduced mortgage insurance costs

Instead of traditional mortgage insurance, this loans use a guarantee fee.

USDA Fees

There are two main fees associated with the program:

1. Upfront Guarantee Fee

- Typically 1% of the loan amount

- Can be rolled into the loan (so you don’t pay it upfront)

2. Annual Fee

- Around 0.35% of the loan balance

- Paid monthly as part of your mortgage payment

Even with these fees, this loans are often more affordable than FHA or conventional mortgages.

Types of USDA Loans Available

There are three main USDA loan programs, but most homebuyers in Indiana use the USDA Guaranteed Loan Program.

1. USDA Guaranteed Loans

This is the most common option.

It’s issued by approved lenders and backed by the USDA. These loans offer:

- Zero down payment

- Competitive rates

- Flexible credit requirements

2. USDA Direct Loans

These loans are provided directly by the USDA and are designed for very low-income applicants.

They may include:

- Subsidized interest rates

- Extended repayment terms

However, income restrictions are stricter than the guaranteed program.

3. USDA Home Improvement Loans

These loans help homeowners repair or upgrade existing homes in rural areas.

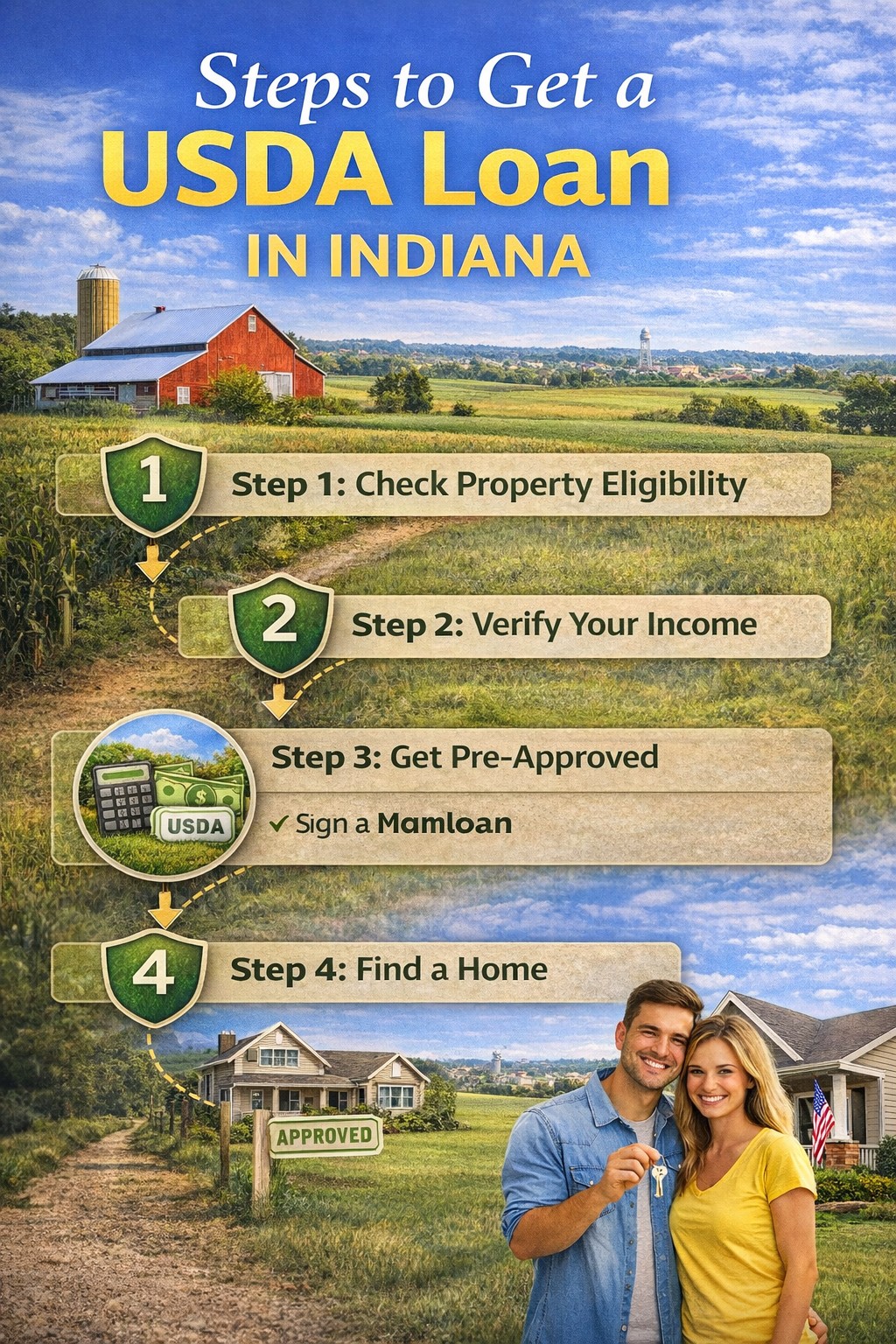

Steps to Get a USDA Loan in Indiana

If you’re considering applying for this mortgage, the process is fairly straightforward.

Step 1: Check Property Eligibility

First, confirm that the home you want to buy is located in a USDA-approved area.

Many lenders can help verify this quickly.

Step 2: Verify Your Income

Next, check that your household income falls within USDA limits for your county.

Remember, this looks at total household income, not just the borrower’s income.

Step 3: Get Pre-Approved

A lender will review your:

- Credit history

- Income

- Debt

- Employment stability

Pre-approval helps determine your budget and strengthens your offer when you find a home.

Step 4: Find a Home

Once pre-approved, you can start house hunting in eligible areas.

Many buyers are surprised by the number of homes that qualify.

Step 5: Final Approval and Closing

After submitting your loan application and completing the appraisal process, your lender will send the loan for USDA approval.

Once approved, you’ll move to closing and officially become a homeowner.

Pros and Cons of USDA Loans

Like any loan program, this loans come with advantages and a few limitations.

Pros

✔ No down payment required

✔ Lower interest rates

✔ Reduced mortgage insurance costs

✔ Flexible credit guidelines

✔ Available to first-time buyers

Cons

✘ Property must be in an eligible location

✘ Income limits apply

✘ Only available for primary residences

For many buyers in Indiana, the benefits far outweigh the restrictions.

Tips for Getting Approved

If you want to improve your chances of qualifying for a USDA loan in Indiana, here are a few helpful tips.

Improve Your Credit Score

Pay down credit cards and avoid opening new accounts before applying.

Even a small score increase can help you qualify for better terms.

Reduce Existing Debt

Lower debt means a better debt-to-income ratio, which lenders like to see.

Save for Closing Costs

While this loans require no down payment, you’ll still need to cover:

- Closing costs

- Inspections

- Appraisal fees

Sometimes sellers can help cover these costs through negotiation.

Work With a USDA-Experienced Lender

Not all lenders specialize in this loans. Choosing one that regularly handles USDA mortgages can make the process much smoother.

Is a USDA Loan Right for You?

If you’re planning to buy a home in Indiana and want to avoid a large down payment, this home loan could be a fantastic option.

It’s especially helpful if you:

- Have steady income but limited savings

- Prefer suburban or rural communities

- Want lower monthly mortgage costs

Thousands of families across Indiana have used this program to become homeowners.

And you could be next.

Final Thoughts

Buying a home is one of life’s biggest milestones, and the process can feel overwhelming at first. But programs like USDA loans in Indiana are designed to make homeownership more accessible.

With zero down payment, competitive interest rates, and flexible requirements, this loans continue to be one of the best options for eligible buyers.

If you’re considering purchasing a home in Indiana, it may be worth exploring whether a USDA loan fits your situation. You might discover that owning a home is closer than you think.